Posted on November 18, 2017 | written by GOONRATHI

Account Dissection

Posted on November 18, 2017 | written by GOONRATHI

Account Dissection

I’m going to point out one error/mistake in the CIG accounts per day.

1.) Geography

In a consolidated set of accounts for a group of companies you eliminate intra-group transactions. This makes sense, because if you sell goods and services between two companies in a group you would just have matching revenue in one company and cost in the other. So in the CIG UK group, you can ignore the revenue in F42, this has an equal expense in CIG UK that you also ignore. You can then ignore the revenue in CIG UK, since this has an equal expense in RSI UK that you also ignore. Essentially you will just be left with the development costs in F42 and the revenue in RSI UK.

RSI UK has one customer. This is Roberts Space Industries, Corp based in the USA. We know that RSI UK invoices in dollars, because they have exchange losses/gains. We know they don’t charge VAT, because they are issuing invoices in dollars to an American company and there is no VAT timing liability on the balance sheet. So we know that the CIG UK group has 100% of its turnover generated in the United States. The accounts however claim that 100% of turnover is attributable to the UK.

These disclosures are typically generated like this by default in an accounting package and it would be up to the accountant to make a manual adjustment to ensure it is correct. It only really affects the overall image of the company rather than any financial implications. If a UK group has 100% turnover in the UK it doesn’t really merit any further thought. If a UK group has 100% turnover in the USA it would make it more obvious that delving deeper showed the entire corporation had one customer and that it was a related party with an almost identical name to one of the UK companies.

If you’re curious why the 2015 comparative figures don’t match, that will be a future error/mistake.

Today’s accounting error/mistake.

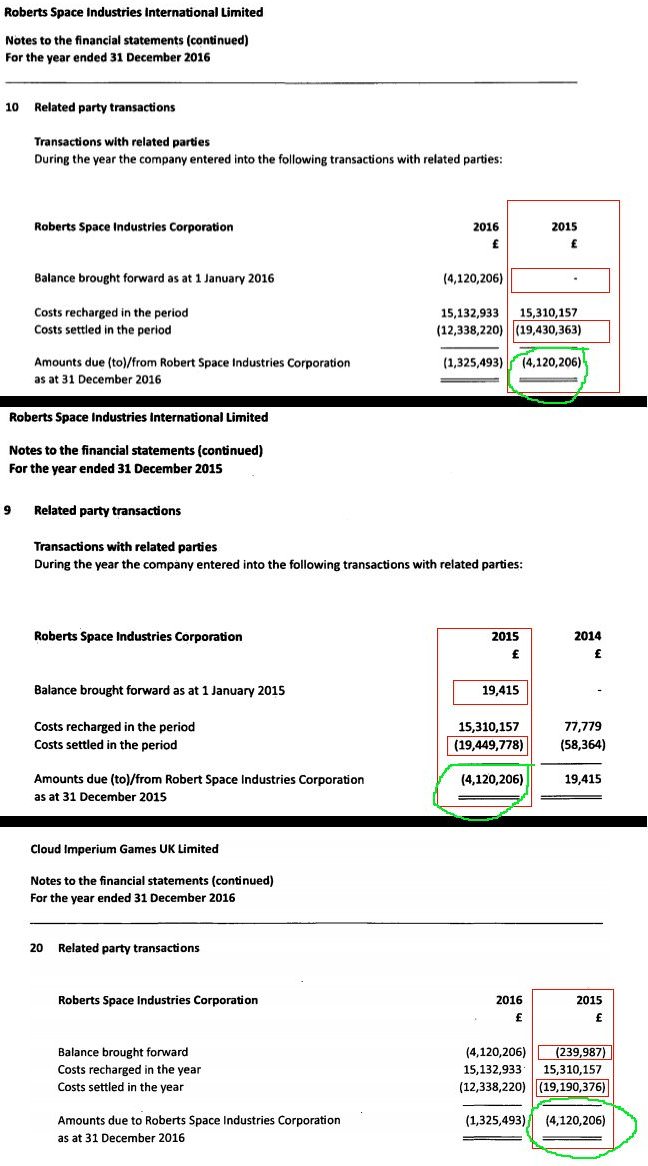

2.) Balance(s) brought forward.

Here I present extracts from three sets of accounts. Roberts Space Industries International 2015 and 2016 and also the Cloud Imperium Games UK Ltd 2016 (consolidated).

All three sets of accounts break down the balance due to Roberts Space Industries Corporation as at 31 December 2015. They all agree that the balance was £4,120,206 due and that costs charged in the period were £15,310,157. All three differ however in the amounts that were settled and that were brought forward from 2014.

At first glance, this would seem to be of little importance. The CIG 2016 group accounts are actually the same as the RSI 2016. While RSI show a bfwd balance of zero, the CIG set are a consolidated amount of zero and of negative £239,987. Ordinarily when preparing the 2016 accounts the 2015 comparatives would be generated automatically from the previous year. This would suggest that the RSI 2015 is the correct breakdown and both sets of 2016 accounts are wrong.

These related party transaction disclosures are usually edited manually, which to me suggests the accountant here is…perhaps not as attention to detail oriented as they could be. My personal opinion is that if you are charging a client some ~£48,000 for two years of accounts, you don’t make basic errors like this. All the client gets to show for your work is 20 sheets of paper, stapled together. So you should always make sure all the sheets are stacked perfectly before and after stapling. You should take a similar level of scrutiny to what is actually printed on the paper.

There is actually a more serious reason this discrepancy and ones like it are annoying and there is a huge “mistake” that is “hidden” here, but I’ll revisit this later.

Today’s accounting error/mistake

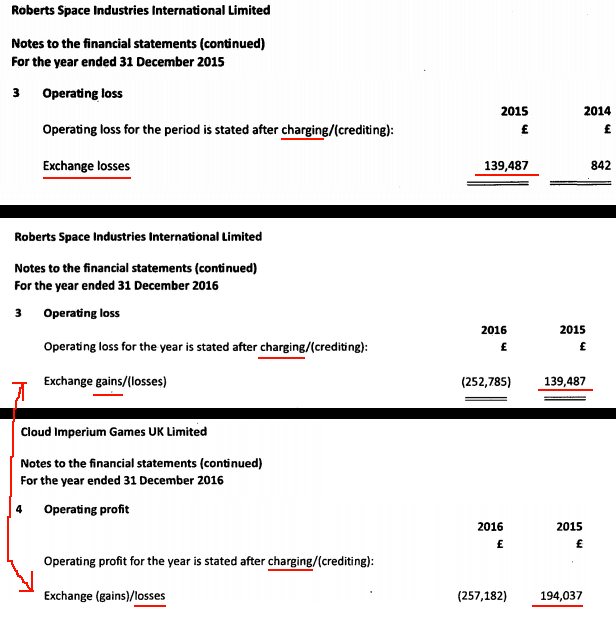

3.) Debits and Credits.

Knowing your debits from your credits may be hard for your first week but this should become pretty ingrained as part of the core of double-entry bookkeeping.

It’s pretty simple. A credit in the profit and loss account is a “good” thing, it increases profit. The corresponding debit in your balance sheet is a “good” thing, it will represent an asset. So a debit value in your profit and loss account will be a “bad” thing that reduces your profit and the corresponding credit in your balance sheet is a “bad” thing that will represent a liability.

So if you make a foreign currency exchange gain, it should be apparent that it will be a “good” thing in your profit and loss account that increases your profit. Thus a credit balance.

So here, you can see the wording is correct in the 2015 RSI accounts. In 2016 someone just had to add “(gains)/.” to the line where it says, “Exchange losses”. Instead they added brackets around the word losses and then added in the gains/ without brackets. This is painful to see because of both how basic the error is and how they had to go out of their way to make the error. I included the line from the CIG UK Ltd 2016 (group) accounts just to show it is possible to get this correct.

This has no real numerical impact but this is building on the narrative about the quality of the preparation of the 2016 RSI accounts, which is some foreshadowing.

Today’s accounting error/mistake is the final one. It builds on the ones that were previously highlighted but this is actually more a series of deliberate decisions. I’m struggling to find a generously innocuous word that conveys making deliberate decisions that are possibly not correct.

4.) Prior year adjustments.

At some point a set of accounts will be filed that are incorrect. Humans can make mistakes. I’ll give an example. Say in 2015 a client paid you in cash for £1000 and you accidentally lost the sales receipt and accidentally banked the money in your personal bank account instead of the company bank account. Later on in 2016, the client asks for a receipt and this helps you remember this event. You’re now faced with three options.

(i) You could file an amended set of accounts for 2015 that makes corrections. This seems intuitive and I’m sure textbooks and “experts” online will tell you this is the right thing to do. No one ever files amended accounts. To be honest I’m not entirely sure why, but it doesn’t happen.

(ii) You can “do nothing”. This doesn’t really mean you do nothing. It means when you file the 2016 accounts, you add on those £1000 sales that were really in 2015 and you pay the company back the cash from your personal account. So now the company is declaring that missing income, albeit in the wrong period.

(iii) You make a prior year adjustment to the 2015 figures in the comparative when you compile the 2016 accounts. You disclose all of these items and you can file an amended tax return, without adjusting the 2015 accounts themselves.

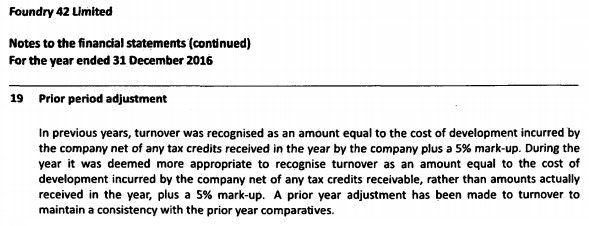

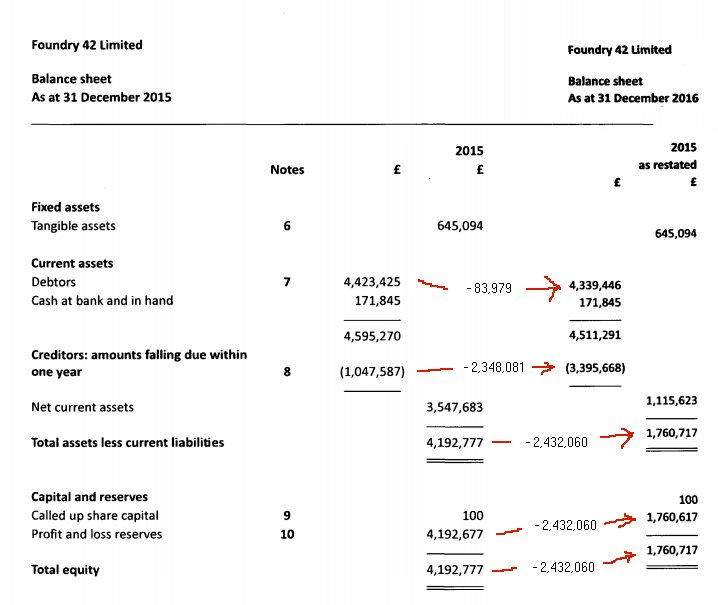

The UK CIG group were faced with such a situation. Here is the disclosure in the Foundry 42 Ltd accounts that explains the decision:

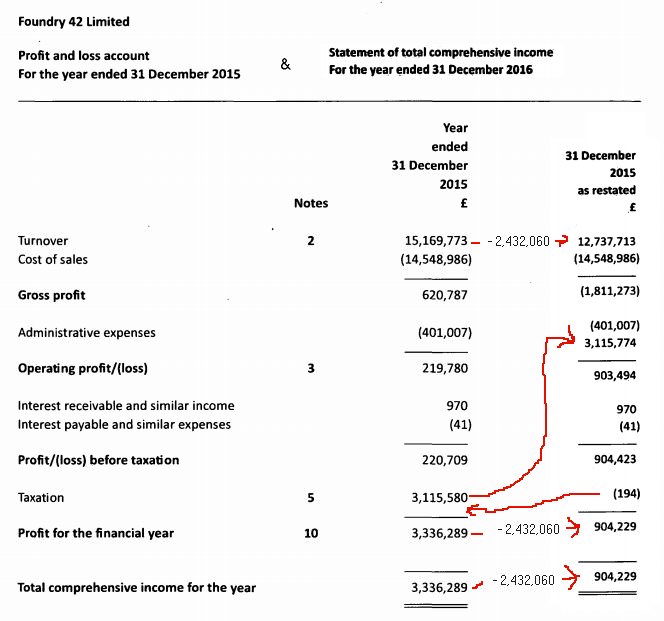

So the original turnover amount was £15,169,773 and it was adjusted to be £12,737,713. A reduction in turnover of £2,432,060. This means they also had to add £2,432,060 to the balance sheet, as a liability. Since they now owed Cloud Imperium Games UK Ltd that amount. You can see they did all this correct (since they were owed £83,979 separately, this is netted off against this amount due to CIG UK).

So far this is all correct from an accounting angle. However, the UK group of companies are all irrevocably linked. Because of the way the accounts were filed, we have access to the individual filings for 2015 but not the group accounts. In 2016 we have the accounts for Foundry 42, RSI and the group accounts (but not the individual accounts for the CIG company). We can pretty much recreate the missing sets of accounts.

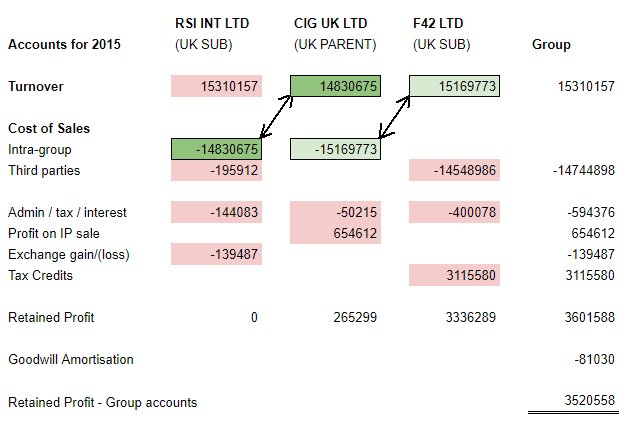

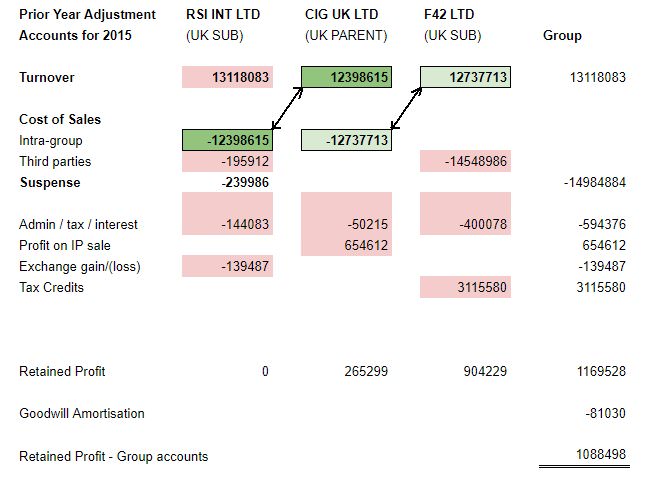

Here is a summary of the 2015 accounts, as they were originally filed. It should be noted that the linked green items, do not appear in the group accounts. These inter-company transactions cancel each other.

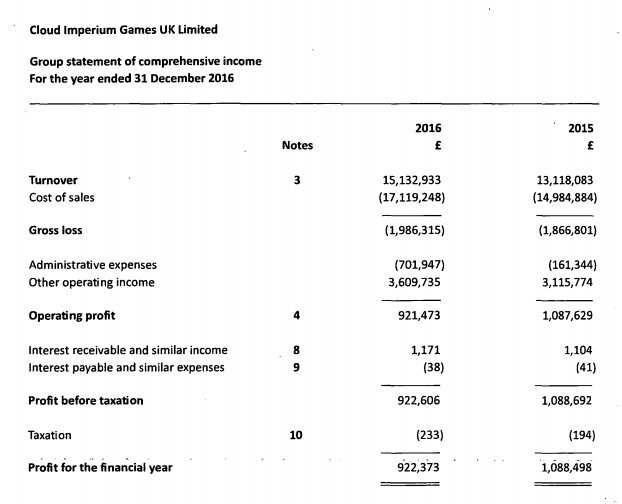

Here is an extract from the 2016 consolidated group accounts. Note the profit for the year 2015 shown as £1,088,498.

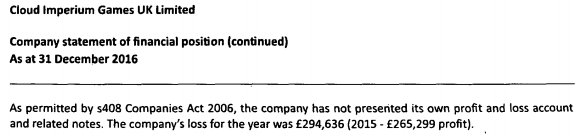

So the group profit in my summary differs from the 2015 group profit that is disclosed in the 2016 accounts by £2,432,060. Now we know what that is, it’s that prior year adjustment. But nowhere in the 2016 group accounts is any prior-year adjustment disclosed. What is disclosed is that the CIG company profit was the same as filed in 2015 at £265,299 profit.

So now we have a big problem. How can we adjust the summary of the 2015 accounts to correct for this prior-year adjustment. Remember all the linked boxes in my summary that can’t be changed individually? If we are reducing Foundry 42s turnover figure by £2,432,060 we also have to reduce CIGs cost of sales by £2,432,060 since that is where the turnover came from. We know that CIG (the company) profit stayed the same though, so we know we have to reduce CIGs turnover, also by £2,432,060. So now we also need to reduce RSIs cost of sales by £2,432,060. All good so far. We know that that RSIs profit remains zero also, because we know the groups profit so we also have to reduce their turnover by £2,432,060 however this goes outside the UK group because this is a refund to Roberts Space Industries Corporation, in the USA. So this is going to be an amount in dollars, so it may not match exactly and we have to rely on the accountants to get this right.

We arrive at a new summary, something like this. Bolded numbers are the figures that have been adjusted:

For some reason, they changed the cost of sales in RSI by adding £239,986 to the costs. I’ve noted it down as a suspense amount because we have no idea why they did this. So to maintain a zero profit, we need to counter this by adding £239,986 to their revenue. This seems like a leap of faith but our summary now matches the group accounts exactly.

So now the group accounts match our summary there are some implications to this. The UK group derives all its income from RSI International Ltd, which derives all its income from the USA company RSI Corporation. Now we can solve why the 2015 turnover figures don’t match and the 2016 ones do match. Note the figure does match our summary for RSI, that we have recreated with our own turnover figure by deduction from the group accounts.

We sort of have to now conclude that there must be two different sets of RSI accounts for them to get this “correct” in the group accounts. The RSI accounts that were filed were never corrected for any prior-year adjustment and yet, there must exist a set of RSI accounts that have been corrected in order to get a set of group accounts that is accurate.

The implications here are decidedly tricky. Back in 2015 the US companies would have presumably filed accounts and tax returns to US authories that claimed a dollar amount of expenses equal to £15.3m. Any audits done at this time, would have confirmation letters and invoices for these amounts. As far as audit trails for this £2.4m refund that would have gone back to the United States, well I hope I have demonstrated that this trail is really unclear for anyone that might investigate it. If it were accidentally paid to the wrong entity and then never declared, there would not be any trail.

So the corrections were handled appropriately in the Foundry 42 Ltd accounts. Adjustments were made and disclosures for those adjustments. They used option (iii) from my opening statement. The CIG accounts are slightly trickier, since we have the company accounts for 2015 and the group accounts for 2016 but we can safely say that some adjustments were made but absolutely no disclosures at all. That is sort of an incorrectly implented option (iii) from my opening statement. The RSI accounts have not had any adjustments made and therefore no disclosures and we have some pretty firm suspicions that there may in fact be two different sets of RSI accounts and they are certainly aware that the filed RSI accounts do not match the RSI accounts used for the consolidation of the group accounts that were filed. So it turns out that there was a hidden fourth option that you will not find in any text books and Chris Roberts has developed new solutions to problems and a way to make money apparently disappear.

I can only imagine the state of the dozen or so American companies that are open to zero public scrutiny.

Unrelated hypothetical paragraph

Imagine your company is sitting on £2.4m in the bank that it should not have, that should be refunded to another company in another country. However, in that country, that company does not know it’s due any money from years ago. It was all audited and balances confirmed at that time and it’s not asking or expecting any money. However, this company with the money in the bank has to get rid of it to make its books balance, it sure should go to the right place and I’m sure anyone would make certain that the right people get this £2.4m.

So as a disclaimer I should stress that I am in no way suggesting that anything unlawful was actually done here. I guess this highlights the “perils” of having multiple shell companies with regard to nice clean audit trails.